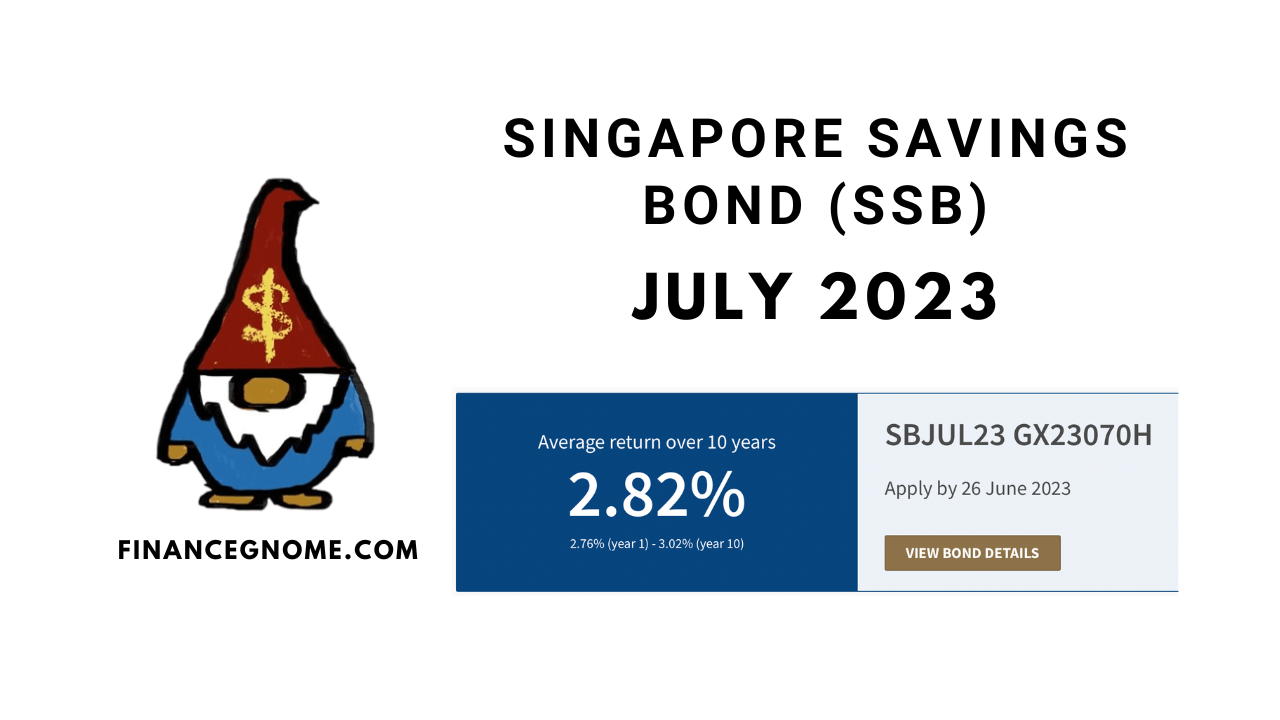

The latest SSB for July 2023 has a 10-year average yield of 2.82%, only marginally higher than last month’s SSB offering 2.81%. The first year yield is 2.76%, and subsequently the yield remains relatively flat but it increases the last few years prior to maturity. This month, there’s $600m on offer. If you’re interested, remember to apply by Monday 26 June, 9pm.

This month’s bond offering is still below 3% average 10-year yield but the yield curve until maturity has started to slope again, as originally intended for this product. SSB was designed to have step up interest rates, i.e. you’re supposed to get higher yield for every year you hold the bond until maturity. However, in recent times shorter-term yields have been higher than longer-term yields, resulting in an inverted yield curve.

If you’re looking for places to park your cash or SRS funds for the long term but still want the option to terminate early without penalty, SSB could be a good option. Unfortunately, SSB is not eligible for CPFIS scheme so you can’t invest your CPF savings into it.

For more details, refer to my Singapore Savings Bond (SSB) tracker.

Why apply for SSB?

In my opinion, the main attraction of SSB is the long tenure while having the flexibility to redeem early without penalty. You’d also still be entitled to accrued interest upon redemption. So if interest rates continue to rise, you have the option of redeeming earlier bonds and applying for the latest issuance with higher interest rates.

Alternatives in Fixed Income

Although one of the safest (backed by Singapore government), SSB is definitely not the highest yielding fixed income instrument in the market. High yield savings accounts, cash funds, fixed deposits and even Treasury bills are yielding higher.

See my Fixed Income Tracker page for info I’ve gathered from various sources on fixed income yields (not exhaustive).

In contrast, if you’re mostly in T-bills or fixed deposits which usually have short tenures and interest rates start to reverse back downwards, you might not be able to find similar high yields when your T-bill or fixed deposit matures.

My thoughts

The Fed has finally paused rate hikes at the last FOMC earlier this month but signalled that they might still raise 2 more times before reaching terminal interest rates. According to the latest Fed dot plot, rate cuts may not come until next year 2024 at the earliest.

Fixed deposit rates offered by banks have been falling, but the latest news seem to be propping up T-bill yields. The last 6-month T-bill auction on 22 June 2023 had a cut-off yield of 3.89%, up from 3.84% at the prior auction.

So far, 10-year SGS bond yields in June (which will be used to calculate August SSB yield) have been on the rise. According to ViresInSolitudine’s calculation, August SSB might yield around 2.97% based on data up to 21 June 2023.

Am I applying this round?

I think SSB below 3% is not yet attractive, but the premium from fixed deposits are narrowing. However, T-bills and cash funds are still offering attractive yields. At the moment, I’m still parking most of my cash in cash funds, and recently in some T-bills.

That said, I always advocate having a mix of longer term SSB and shorter term FD, T-bills, cash funds, or even high-yield savings accounts for emergency funds or the cash portion of our portfolio.

Currently, I’m sitting on $40k SSB which are my emergency funds. The rest of my spare cash is mostly with MoneyOwl WiseSaver (yielding 4.18% based on 5-day Moving Average as of 16 June 2023) while waiting for other opportunities.

My allocations to SSB have been fully optimised at yields above 3% so I won’t even consider applying for SSB probably until yields move above 3%.

Will you be applying for this July SSB?

Follow me on Facebook, Telegram, Twitter and Youtube.

Disclaimer: This is not financial advice. I am not professional financial advisor nor do I work in the finance industry. Anything I write here is purely my personal opinion. Please do your own research and due diligence before investing into anything. All investments come with associated risks. Best to consult a financial advisor if you’re still unsure.

Download my FREE Ebook: How to Start Investing in Stocks for Beginners

For more investing tips, visit my Guide page.

- Standard Chartered Online Trading: Referral link

- FSMOne: Referral code P0267058

- Tiger Brokers: Referral link | Review

- Futu SG (moomoo app): Referral link | Review

- Webull: Referral link

- Syfe Wealth & Syfe Trade: Referral code FINANCEGNOME | Referral link | Review

- Endowus: Referral code J5HPB | Referral link

- CoinHako: Referral link

- Crypto.com: Referral link

- Portseido: Referral link

For more investing resources, see my Referrals page.

Disclosure: This post may contain affiliate links and I may get a commission when you click on the links or open an account through the links, at no additional cost to you. I only recommend products or services that I have personally tried and have found useful.

One thought on “Singapore Savings Bond (SSB) July 2023 – Yield Curve Normalising Slightly, Wait For Higher Yields”

Comments are closed.