Grab Holdings announced on 13th April 2021 their intention to go public via reverse merger with US-listed SPAC (special purpose acquisition company) Altimeter Growth Corp (Nasdaq: AGC) at a whopping valuation of ~$40B

I’m excited about this deal because Grab is only the second tech unicorn from Southeast Asia in recent times to go public since Sea Limited (Nasdaq: SE) did so in 2017.

In today’s post, I’ll be covering some key highlights on the deal (from the investor presentation here) and share my initial thoughts. This won’t be a deep dive, but do subscribe and let me know in the comments if you enjoyed this post and would like me to take a closer look at Grab.

If you prefer to watch a video, I’ve also created one on YouTube.

| Contents 1. Company overview 2. Transaction overview 3. My initial thoughts 4. What I’m doing |

Company Overview

If you’re living in Southeast Asia or have visited the region recently, you might be familiar with Grab. Grab is the leading super app in Southeast Asia, and is ranked #1 in the region in all 3 of its operating segments by GMV (gross merchandise value).

Grab’s super app offers a myriad of services to cater to everyday needs. They started with Mobility which is the ride-hailing business, and expanded into Deliveries including food, groceries, and parcel deliveries. In addition, Grab also offers Financial Services mainly through Grab Financial Group, including payments through GrabPay e-wallet and GrabPay card, Insurance, Investments, Loans, Remittance and PayLater.

Grab’s 3 main segments are Deliveries (~50% of revenue), Mobility (~30% of revenue) and Financial Services (~20% of revenue). Grab operates in 8 countries in Southeast Asia, namely Malaysia, Singapore, Philippines, Thailand, Vietnam, Cambodia and Myanmar.

Grab is essentially a platform connecting 5+ million driver partners and 2 million merchant partners with its 25 million monthly transacting users or consumers.

In 2018, Grab acquired Uber’s business Southeast Asia. Just last year in 2020, Grab was awarded one of only two digital full banking licenses in Singapore, the other one going to Sea Limited. Grab had also previously held merger talks with its main Indonesian ride-hailing rival, Gojek but the deal didn’t materialized.

In terms of financials, Grab is projecting to grow GMV (gross merchandise value) and revenue in excess of +40% CAGR from 2020 to 2023, essentially almost tripling in the span of 3 years. Grab expects its Deliveries and Financial Services segments to grow much faster than its Mobility segment.

However, profitability is not expected to come until end 2023 in terms of EBITDA. Grab didn’t provide any net loss/profit projections, but reported a net loss of $2.7B in 2020.

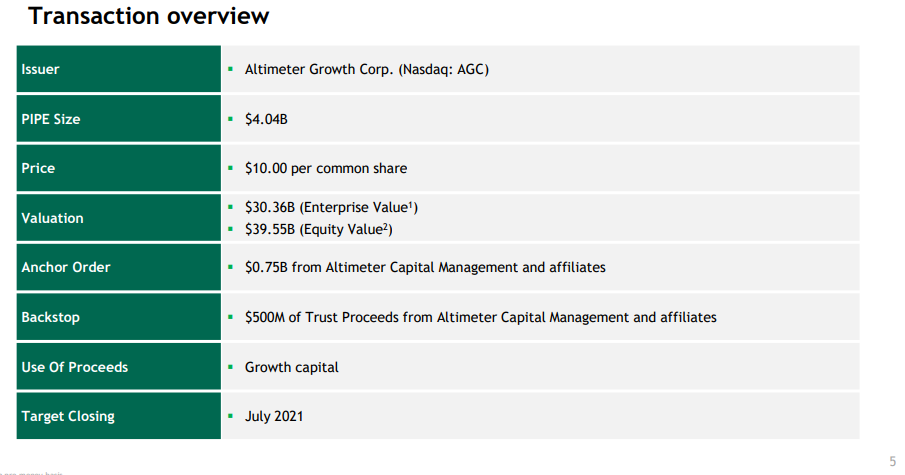

Transaction Overview

Grab intends to merge with SPAC Altimeter Growth Corp (AGC) and upon closing, will be traded on the Nasdaq under ticker GRAB. Pro-forma equity value will be $39.6B and pro-forma enterprise value will be $30.4B. Grab is expected to receive $4.5B in cash proceeds, including $4B in fully committed PIPE (private investment in public equity) offering.

The PIPE investor roster is impressive, with big institutional names like BlackRock, T.Rowe Price, Fidelity, and Temasek among others. Altimeter has committed to a 3-year lock-up period for its sponsor promote shares, which is testament to their long-term commitment to Grab.

Shares are priced at $10 per common share for insiders and PIPE investors. Retail investors like myself will have to buy shares from the open market under ticker AGC (prior to deal closing) or GRAB (after deal has closed).

The reverse merger deal is targeted to close by July 2021. Between now and then, it is not a done deal and there’s still a possibility the transaction doesn’t go through. Both Grab and Altimeter have to gain approval from their respective shareholders.

My Initial Thoughts

I love Grab’s business and I’ve been waiting for them to go public for the longest time. I like Grab’s super app strategy and believe that they will continue to dominate Southeast Asia’s delivery and ride-hailing scene. By creating an ecosystem of complementary services addressing high-frequency everyday needs all through one app, Grab is banking on the stickiness factor to keep consumers in their app and spending more. I really like platform technology companies that provide value to both ends, to the driver/merchant and to the consumers.

Grab has also achieved a flywheel effect, where as more consumers use their app, that attracts more driver and merchant partners onto their platform, thus consequently providing more value to consumers and in turn attracts even more consumers.

Investor appetite for Southeast Asia startups seems to be increasing as well, the best example being Sea Limited also listed in the US, whose price has surged in 2020 and is now trading at a valuation in excess of $120B.

However, I do have my reservations on the valuation and the SPAC vehicle that Grab is taking to list.

On valuation, Grab is valued at a pro-forma P/S of 25x (at $10/share) by early investors. For retail investors however, we will likely be paying a premium which is anything above $10. At the time of writing, AGC share price is around $13/share which is a 30% premium. Thus, if you buy AGC now, you are effectively valuing Grab at roughly $52B and at P/S 33x. However, if you believe that Grab can hit its projected revenue of $4.5B by 2023, the P/S will drop to around 12x. In comparison, Sea Limited (SE) is currently valued at P/S 30x.

On listing via SPAC, I don’t fully understand why Grab chose the SPAC route instead of the traditional IPO route. Unlike many other startups that merge with SPACs that are pre-revenue, Grab has a proven business model, already generating revenue, and demonstrating rapid growth. If they had chosen the IPO route, I’m confident their offering would be well received and in high demand.

From my research, SPACs provide advantages in terms of speed to market (roughly 3-6 months vs up to a year for IPO) and more certainty on funds raised from the transaction. Investing in a SPAC prior to deal closing is also very risky because retail investors usually pay a premium and there’s a chance that the deal might not materialize. Most SPACs seems to also not do well post-merger, but that might partly be due to the SPAC hype and frenzy pushing up prices last year.

That said, Altimeter has shown great confidence in Grab by committing to a 3-year lock up period, committed substantial amounts of their own funds to the PIPE, and agreeing to Founder and CEO Anthony Tan having 60% voting power post-merger. These additional sweeteners might have swayed Grab towards this SPAC deal instead of an IPO.

Practically as a foreign investor to US markets, buying a SPAC is an opportunity to get shares into a company prior to it going public. In Singapore, we don’t have much access to US IPOs except maybe through certain US brokers (I’m not too familiar with the process of applying for US IPO from Singapore, never done it before).

From a longer term perspective, an important consideration is Grab’s path to profitability. Investors need to keep a close eye on how Grab tracks against their projections especially in the following quarters post-merger.

What I’m Doing

Although Grab’s valuation coming out of this SPAC deal is certainly not cheap, it does come with rapid growth. If Grab continues on this growth trajectory and continues to execute, I can see a Grab possibly fetching a valuation of $100B in 3-5 years’ time – which translates to ~$25/share. That would be almost double from AGC’s price today of ~$13.

However, I’m not in a rush to jump in and willing to wait until the SPAC hype dies down. Also, I’m still down substantially on the 2 previous SPACs I had invested in. So I’ll probably wait for a better entry point maybe below $12. Alternatively, I might just initiate a small starter position and monitor developments closely before putting in more money.

Thanks for reading! Are you vested or do you intend to invest in Grab? Before or after merger closing? Let me know in the comments.

References

Disclosure: I’m long Sea Limited SE

Disclaimer: This is not financial advice. I am not professional financial advisor nor do I work in the finance industry. Anything I write here is purely my personal opinion. Please do your own research and due diligence before investing into anything. All investments come with associated risks. Best to consult a financial advisor if you’re still unsure.